The financial markets are currently experiencing a shift in the roles of traditional safe-haven assets. Gold, traditionally seen as a hedge against inflation and market volatility, is now being treated more as a strategic reserve asset. On the other hand, the Japanese yen, long regarded as a safe-haven currency, is undergoing a transformation where its haven status is now conditional. This shift in the “New Haven Hierarchy” is creating a complex macro environment, where both gold and the yen can rise in value at the same time, despite their traditionally opposing behaviors in times of economic stress.

KEY TAKEAWAYS

- Gold’s New Role: Gold is increasingly treated as reserve collateral with no counterparty risk, driven by geopolitical risk and central bank demand.

- Yen’s Conditional Haven Status: The yen’s role as a safe-haven asset is now conditional, influenced by Japan’s monetary policies and fiscal dynamics.

- USDJPY Paradox: USDJPY can rise even as JGB yields increase, driven more by relative policy divergence than traditional yield expectations.

- Gold and Yen Divergence: Gold and yen are behaving differently in this regime, with gold acting as a hedge while the yen serves as a funding currency.

- Positioning Implications: Investors may consider holding long gold and using the yen as a funding currency until a significant policy change occurs.

Japan’s Exit from NIRP: A Shift with Limited Immediate Impact

In March 2024, Japan exited its Negative Interest Rate Policy (NIRP), raising its policy rate to 0.0%-0.1%. While this move marks a significant policy change, the immediate impact on Japan’s currency and economic dynamics has been muted. Japan remains a low-yield environment compared to the U.S. and other developed markets, which continues to make the yen an attractive funding currency for global investors.

The end of NIRP reduces the risk of prolonged dovish policies, but it does not change the structural incentives for investors to engage in “borrow JPY, buy higher yield” strategies. The yen continues to behave like the world’s cheapest balance sheet, maintaining its role as a funding currency until there are significant policy changes or external shocks.

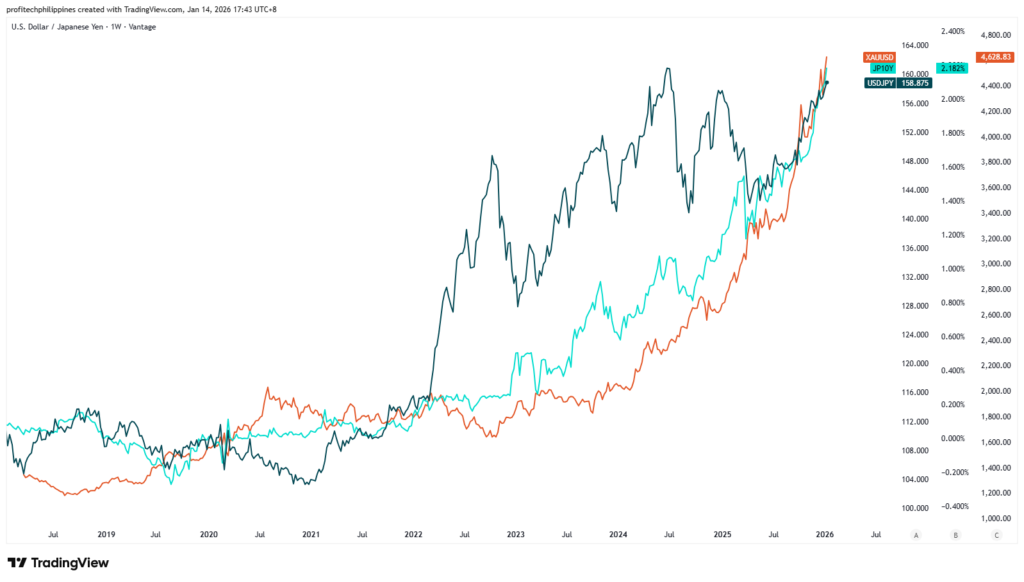

Why USDJPY Can Rise Even as JGB Yields Increase

Traders often assume that higher Japanese Government Bond (JGB) yields should lead to a stronger yen. However, recent trends have shown that this relationship is not always straightforward. In 2026, there were instances where rising JGB yields coincided with yen weakness, driven more by fiscal and political uncertainty in Japan than by tightening monetary policy.

Higher yields in Japan reflected risk premiums rather than a sign of tightening, leading to capital outflows and increased demand for the U.S. dollar. As a result, USDJPY rose even as JGB yields increased. This highlights the complex nature of the yen’s behavior, influenced by both domestic factors and global macroeconomic trends.

The Yen’s Conditional Haven Function

The yen’s role as a safe-haven was historically rooted in Japan’s external balance, its net creditor position, and the unwinding of yen shorts during risk-off events. However, in the current macro environment, the yen behaves more like a funding currency, influenced by Japan’s low yields and policy divergence with the U.S.

While the yen can still function as a safe-haven during sharp risk-off events, its behavior is now conditional, depending on the broader macroeconomic context. The dominance of carry trades and policy divergence has weakened its automatic haven status, making it more of a regime-dependent asset rather than a constant safe-haven.

Gold’s Shift from Inflation Hedge to Reserve Collateral

Gold’s role in the global financial system is evolving. Traditionally seen as a hedge against inflation and a store of value during times of market instability, gold is now increasingly viewed as a strategic reserve asset. Central bank demand for gold reached record highs in 2024, with gold becoming the second-largest global reserve asset after the U.S. dollar.

This shift is largely driven by concerns over geopolitical risk, asset freezes, and sanctions. As a result, gold is being treated as a non-counterparty-risk asset, offering a hedge against political and financial instability. In this new macro regime, gold is viewed not just as a hedge but as a crucial component of central banks’ reserve buffers.

The Cross-Asset Correlation: USDJPY, JGB Yields, and Gold

In the current macro regime, gold, the yen, and JGB yields are interconnected in ways that create a seemingly paradoxical market.

- JGB Yields: The rise in JGB yields reflects both Japan’s policy normalization and increased fiscal/political risk.

- USDJPY: The relative carry trade continues to support a weaker yen, driven by the policy differential between Japan and the U.S.

- Gold: Official-sector demand and geopolitical risks are pushing gold prices higher as a strategic reserve asset.

These three assets—JGB yields, USDJPY, and gold—can rise together in this regime, driven by relative pricing of money, risk premiums, and demand for safe-haven assets. This creates a surface-level positive correlation between them, even though the underlying market dynamics are more complex and regime-dependent.

Positioning Implications in the New Haven Hierarchy

For institutional investors, the current macro regime calls for a “barbell” strategy: holding long gold exposure as reserve collateral and tail hedge, while using the yen as a funding currency until a significant catalyst forces a reversal. This strategy involves maintaining gold as a long-term hedge against geopolitical and financial risks, while respecting the short-term pain trades in USDJPY, particularly when the market is crowded with short yen positions.

The key to success in this environment is flexibility and responsiveness to the evolving macroeconomic landscape, staying prepared for potential policy shifts or global deleveraging.

Macro Signposts to Monitor

To navigate this evolving macro regime, investors should monitor the following indicators:

- U.S.-Japan Rate Differential Expectations: Track the front-end and 2Y/5Y yield spread for insight into future policy moves.

- JPY Basis/FX Hedge Costs: Watch for constraints on foreign demand for Japanese bonds, which can affect the yen’s funding costs.

- Japan’s Fiscal Impulse/Election Risk: Japan’s fiscal policy and election outcomes can have significant effects on the yen’s value.

- Central Bank Gold Commentary: Monitor central bank actions and commentary related to gold accumulation.

- Geopolitical Risk: Track geopolitical events that might drive gold prices higher and influence yen behavior.

Conclusion

The shift in the “New Haven Hierarchy” is reshaping how investors view gold and the yen. Gold is being redefined as a strategic reserve asset, driven by central bank demand and geopolitical risk, while the yen’s role as a safe-haven is now conditional, impacted by Japan’s evolving policies. Understanding these changes is essential for navigating the current macroeconomic environment, where gold and the yen can rise in value together despite their traditionally opposing roles during times of financial stress.