A weekly market update helps traders understand how the forex market behaved over a short period of time. Instead of focusing on predictions, it explains how prices reacted to news, sentiment, and expectations. During the week of January 19 to January 25, trading activity was shaped mainly by political headlines, central bank credibility, and inflation updates. This update explains what moved markets last week and why traders remained cautious heading into another event heavy week.

KEY TAKEAWAYS

-

Last week was driven by politics and central bank messaging

-

Gold rose by about eight percent while the US dollar fell by about two percent as traders sought safety

-

Risk appetite stayed uneven as uncertainty remained high

-

Inflation cooled in some regions but did not remove political risk

-

The biggest risk this week comes from the Federal Reserve decision and tone

TLDR SUMMARY

Last week showed a clash between easing inflation signals and rising political noise. Traders focused more on protecting capital than chasing returns. Safe assets gained while confidence in policy stability weakened. This week places central banks back at the center of market attention, especially the tone from the Federal Reserve.

What Happened Last Week

Davos and Political Headlines

Global political discussions dominated market thinking throughout the week. The tone from international leaders leaned more toward power politics, trade pressure, and policy credibility than growth optimism. Markets tend to struggle when rules and direction feel unclear.

Risk mood stayed mixed but leaned defensive. Traders favored protection over aggressive positioning. Gold climbed sharply as demand for safety increased. The US dollar weakened as confidence in policy stability wobbled. Stocks finished slightly lower as risk was trimmed into the weekend.

Inflation Updates Across Major Economies

Inflation data from the euro area, Canada, and the United Kingdom suggested cooling price pressure. Lower inflation can reduce the need for future rate hikes, which briefly supported risk appetite.

This support was not clean or lasting. Political uncertainty kept traders hedged. The euro found mild support as inflation cooled and expectations steadied. The British pound reacted more sharply to inflation, jobs, and retail data than usual. Gold remained supported because easing inflation did not remove broader uncertainty.

China Growth Data

Early in the week, China released a group of economic data that pointed to steady growth. The data did not signal overheating or sharp weakness.

This helped calm fears of a hard landing and gave mild support to commodities and Asian risk assets. The Australian dollar and regional markets saw early week support. Confidence improved slightly but did not turn optimistic.

US PCE Inflation

US personal consumption inflation remained firm. This matters because it is the preferred inflation gauge of the Federal Reserve.

Sticky inflation reduces the chance of quick rate cuts. That pressure tends to weigh on stocks and crypto. Even so, US dollar weakness continued because political risk mattered more than one data point.

Bank of Japan Decision

The Bank of Japan held policy steady. What caught market attention was internal disagreement.

Even limited dissent matters because Japan is a major funding currency. Small shifts in expectations can move currency markets. The yen reacted to the signal, and dollar yen trading stayed volatile as the US dollar weakened.

US Consumer Sentiment

US consumer sentiment improved slightly late in the week. A better mood can support spending, which matters for growth.

The impact was brief. One survey was not enough to offset political noise and central bank uncertainty. Risk assets still ended the week cautiously.

What to Watch This Week

Federal Reserve Decision and Tone

The upcoming rate decision is expected to hold policy steady. The focus will be on language rather than action.

Markets will listen closely for how the Fed talks about inflation progress, growth risks, and independence. The hour around the statement and press conference often brings sharp moves in the US dollar, gold, equities, and crypto.

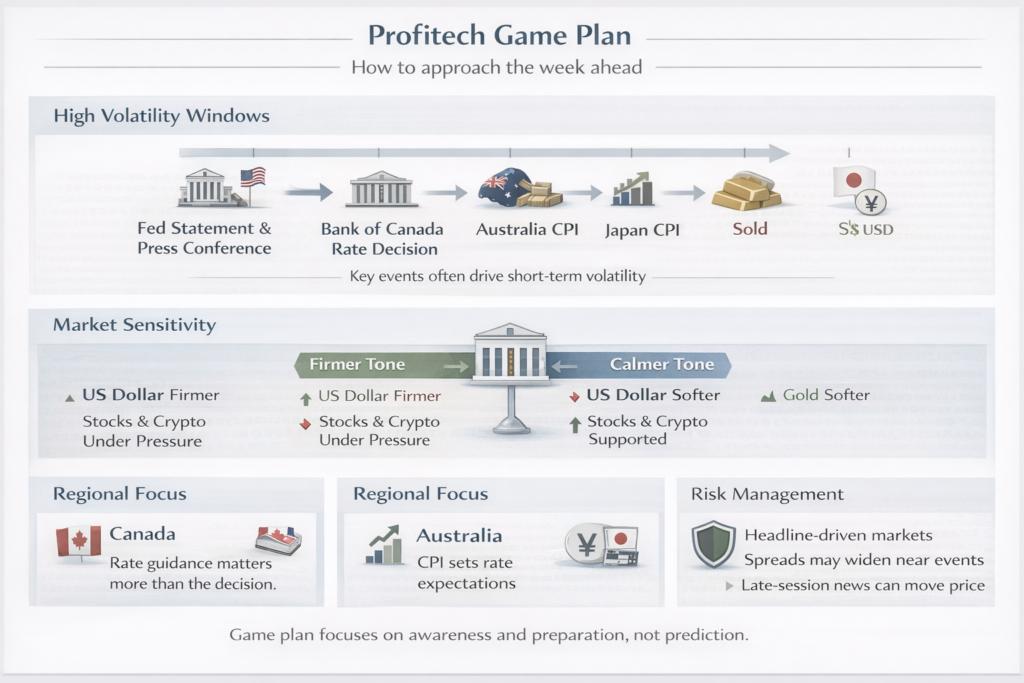

Bank of Canada Decision

The Bank of Canada is also expected to hold rates. Canada is highly rate sensitive because housing and consumer spending respond quickly.

Guidance matters more than the decision itself. A signal that tightening is finished may weaken the Canadian dollar. A reminder that hikes remain possible could trigger sharp moves in USDCAD and oil linked pairs.

Australia Inflation Data

Australia inflation remains the main driver for the Australian dollar. Frequent updates shape expectations for the Reserve Bank of Australia.

Hot inflation may support the currency and raise rate expectations. Cooler data may ease pressure and weigh on the Australian dollar. Australian equities and metals tied to China demand often react as well.

US Durable Goods and Consumer Confidence

Durable goods data reflects business spending on large equipment. Consumer confidence reflects how households view future spending.

Weakness in both can raise growth slowdown concerns. Stability in both can support the view that current policy levels remain manageable.

Japan Inflation

Japan inflation helps shape expectations for future policy change. Firm inflation may raise expectations for tighter policy and support the yen. Softer readings may limit that support.

Davos Aftershocks

Political headlines can continue to influence markets well after global meetings end. Statements, deals, and trial ideas can surface days later. These headlines can override scheduled data in the short run.

Profitech Game Plan

-

Identify high volatility windows around central bank decisions and inflation data

-

Treat markets as headline sensitive throughout the week

-

Use liquidity caution since spreads may widen during policy events and late sessions

If the Federal Reserve sounds more focused on inflation risk, markets may lean toward a stronger US dollar, weaker stocks and crypto, and softer gold. If the tone leans toward growth concern or inflation comfort, markets may lean toward a weaker dollar, firmer risk assets, and stronger gold.

Hotter inflation in Australia may support the Australian dollar. Cooler readings may pressure it. Firmer inflation in Japan may support the yen as markets adjust expectations for future policy changes.

Disclaimer: This content is for informational and educational purposes only and does not represent financial advice. Trading involves risk, and market conditions can change quickly. Always conduct your own analysis or consult a qualified professional before making trading decisions.